Unfortunately, payments and bills are still due even if you’ve experienced financial hardship in the wake of COVID-19. Debt management looks a little different during a crisis, but the essentials are still there — avoid late payments, put down as much as you can afford, and focus on certain debts over others.

Crisis situations are the ultimate times to re-evaluate your “needs” and “wants.” You have to ask one question about new purchases and ongoing expenses right now: “Can I live without this?” Everyone’s answers are unique. Maybe you can do away with your streaming services if you can’t afford living expenses — there is always free streaming content, jigsaw puzzles, and books that can entertain you and your family while you’re getting back on your feet. It’s possible, though, that Disney+ is keeping you sane with children at home, or your wellness app is keeping you centered. Your well being and saving your credit score for the future are your top priorities in a crisis. In this post, we’re offering a guide for what to pay first and what you can do for relief.

Mortgage & Rent

Housing expenses should be your highest-priority payments. Your most important goal is having a safe place to live and keeping a home in which to shelter. While many states have put eviction freezes in place, you’re not completely off the hook. Failing to pay rent or mortgage can still result in eventual foreclosure or eviction; the freeze only makes it so you can’t be evicted right away. You may end up having to pay all of the back-logged rent at once when this is over. Keep up with your payments if possible and work with your landlord or mortgage lender to come to a deal that won’t leave you stacked with late payments when the freezes are lifted.

Housing expenses should be your highest-priority payments. Your most important goal is having a safe place to live and keeping a home in which to shelter. While many states have put eviction freezes in place, you’re not completely off the hook. Failing to pay rent or mortgage can still result in eventual foreclosure or eviction; the freeze only makes it so you can’t be evicted right away. You may end up having to pay all of the back-logged rent at once when this is over. Keep up with your payments if possible and work with your landlord or mortgage lender to come to a deal that won’t leave you stacked with late payments when the freezes are lifted.

Household Utilities

Stay up to date with your water, sewer, electric, and gas. You don’t want to accrue fees that might bar you from energy assistance programs or shut off your utilities entirely, making it that much harder to stay healthy at home. If you’re having trouble making payments, reach out to your utility providers — many have hardship assistance programs and deferred-bill options.

Car Payments

Your car payments should remain your highest priority after your home expenses. You’ll want to avoid a repossession at all costs — you need that car for essential errands and getting to work when life returns to normal. Luckily, most major auto brands are offering payment deferrals and waiving late fees. Contact your lender to discuss how you can keep your account in good standing. While it may be tempting to cancel auto insurance, doing so can raise your rates later and leaves you open to serious expenses if your car suffers storm damage or is stolen while parked. If you don’t own your car outright, cancelling insurance isn’t an option. Many auto insurance companies are offering refunds on premiums paid during COVID-19. You should be able to work with your insurance company to reduce your rates during this time.

Credit Cards & Other Debts

Your other debts shouldn’t have such a direct impact on your health and safety, and therefore can be renegotiated right now — medical bill and back taxes, for example.

Your other debts shouldn’t have such a direct impact on your health and safety, and therefore can be renegotiated right now — medical bill and back taxes, for example.

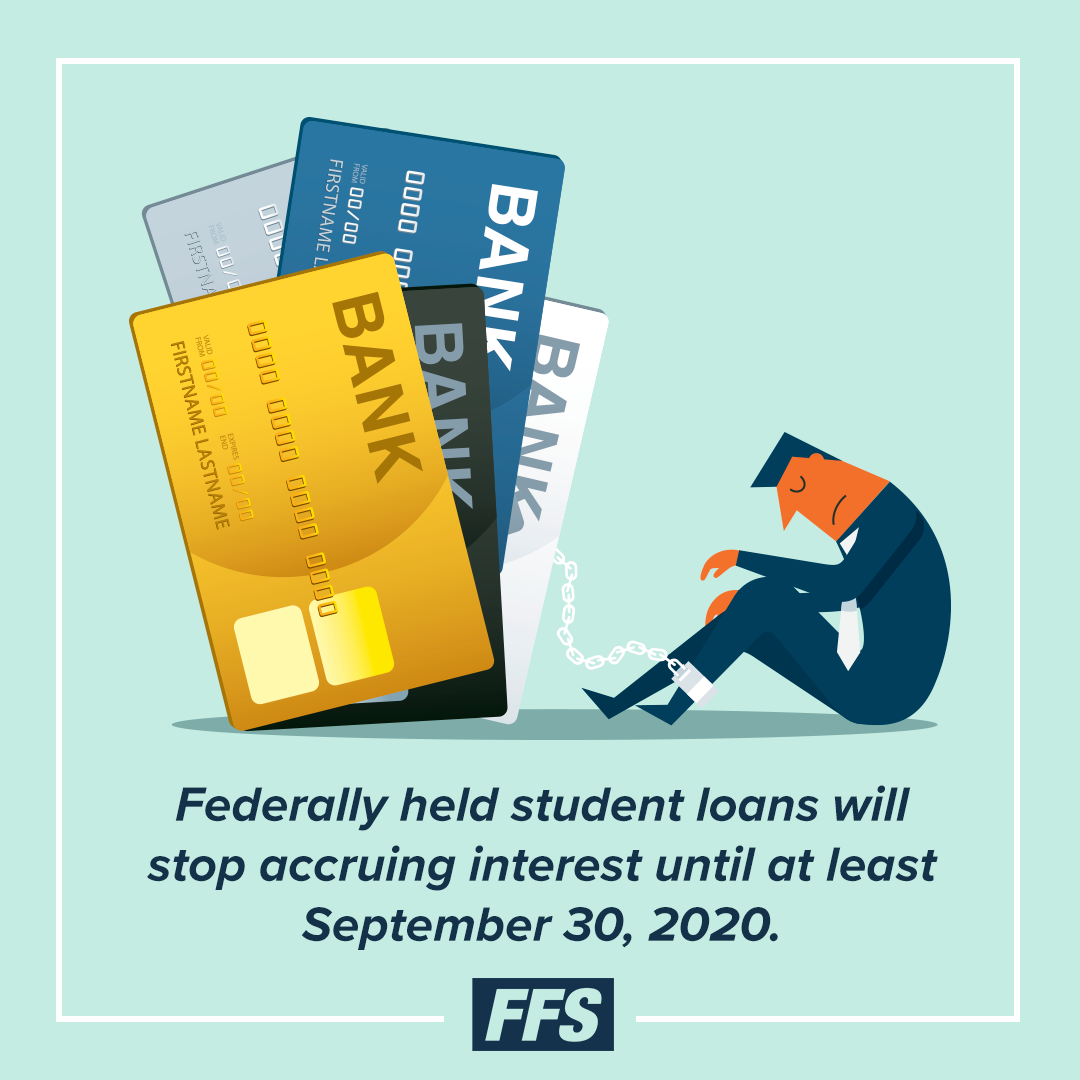

Thankfully, the government has mandated that all federally held student loans will stop accruing interest until at least September 30, 2020. You do not need to do anything to take advantage of the 0% interest. Do not pay anyone who offers to reduce your federal student loan interest rates for a fee. The 0% interest does not, however, apply to private student loans – negotiate with your loan officer for support.

As for credit cards, most major banks are letting their borrowers defer for now. Many are also refunding certain fees and altering minimum payments. For reference, there is a list of relief-options offered by different card carriers. You’ll have to call your specific lender to take advantage of these provisions, however. Ask them directly what they can offer in terms of deferment and other measures of assistance.

Stay on Track

Remember that ignoring your debt is never a good idea. If you can’t cover a bill, confront it — contact the lender or creditor and let them know the crisis has changed your ability to make a payment. They’ll likely be willing and ready to make an arrangement with you due to the unprecedented nature of this crisis. You have options. Take a deep breath — with planning, you can prioritize your debts and keep your credit under control. For more information on paying off debt, check out our latest Focus on YOUR Money webinar here*.

Read our other articles in the Focus on YOUR Money series to get tips on saving, budgeting, and how to improve your credit score.

* Webinars are available to current FFS Agents.

FFS Agents – share this blog with your networks using our resources in the ABO.